Let’s begin with some highlights from the last week:

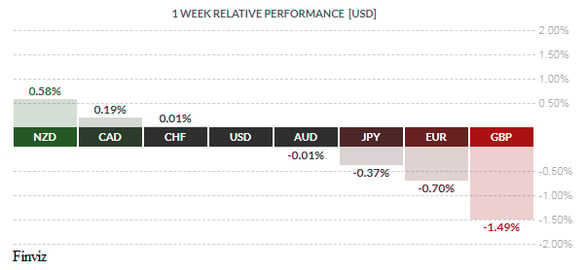

- The best performing currency last week was the NZD due to upbeat comments by RBNZ Governor Orr. He said that “unconventional policy is unlikely” because the “cumulative impact of easing is working its way through the economy”. That seems to be code for “QE is unlikely”.

- On the flip side, the GBP was at the rear of the currency pack due to dovish comments by a traditional hawk at the Bank of England who indicated that even a smooth Brexit may not be enough to prevent the Bank of England from lowering interest rates.

- A smooth Brexit is still unlikely since Prime Minister Johnson continues to say he will refuse to request a three-month Brexit extension as instructed by Parliament.

- Japan’s manufacturing PMI contracted for a fourth consecutive month and to its lowest level since June 2016.

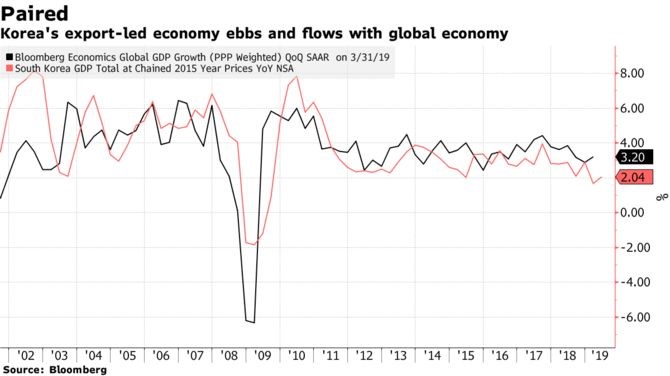

- South Korean Exports collapsed by 21%, the biggest drop in a decade, due to Trump’s trade war and trade tensions with Japan.

- The euro hit new lows for the year on a disappointing flash PMI. Eurozone Markit Composite PMI (Sep) Prelim fell from 51.9 to 50.4. It was the lowest composite reading in 75 months and is beginning to look more and more like levels consistent with the 2012 recession.

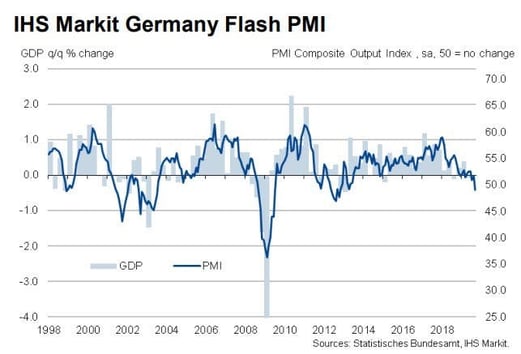

- Meanwhile, the powerhouse of the Eurozone economy, Germany, continues to weaken. Flash Germany PMI Composite Output Index fell to 49.1, an 83-month low.

- Citibank's Economic Surprise Index has reached an 18-month high and Bloomberg Economic Surprise Index has reached an 11-month high. This means that economic data is coming in better than expected, which also helps to explain why the Fed’s rate cutting outlook has cooled with their last hawkish cut.

- The growth divergence between the US and the Eurozone helps to explain why the USD dollar index, which has euro weighting of 57.6%, refuses to break down despite two rate cuts by the Fed.

The month of September has been a bad month for politicians: Prime Minister Boris Johnson (Supreme Court reverses prorogation of Parliament), Justin Trudeau (blackface pictures), and now President Trump, who is now the subject of a formal impeachment inquiry. We won’t wade too deeply into politics here, but we will stay tuned to this fast-moving scandal to see how it may impact global markets.

The economic calendar in the week ahead is a busy one, but don’t be surprised if political uncertainty takes center stage. In the US, the latest readings of both the labor market and consumption will be announced. Neither reading should dissuade from what is essentially a 2% growth economy. With last week’s terrible PMI reading out of the Eurozone, all eyes will be on this week’s PMIs for China (Monday) and the US (Tuesday). Other data to watch out for is Canada’s GDP on Tuesday, US Non-Manufacturing PMI on Thursday, and Canada’s Ivey PMI and International Merchandise Trade on Friday.

The third quarter officially ends on Monday, so portfolio re-balancing from fund managers may provide extra volatility. The first day of October brings three events into focus: China celebrates 70 years of Communist rule, Japan's sales tax will be increased to 10% from 8%, and a rate decision will be delivered from the Reserve Bank of Australia. The market sees an 80% chance of a quarter point rate cut to a new record low of 0.75%. If this doesn’t materialize, the market will likely react more violently.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, SEPTEMBER 30 | ||||

| 04:30 | GBP | Current Account | -19.2B | -33.1B |

| 17:00 | NZD |

NZIER Business Confidence

|

-34 | |

| 21:30 | AUD |

Building Approvals m/m

|

2.1% | -9.7% |

| TUESDAY, OCTOBER 1 | ||||

| 00:30 | AUD | Cash Rate | 0.75% | 1.00% |

| 00:30 | AUD | RBA Rate Statement | ||

| 05:20 | AUD | RBA Gov. Lowe Speaks | ||

| 08:30 | CAD | GDP m/m | 0.1% | 0.2% |

| 10:00 | USD | ISM Manufacturing PMI | 50.4 | 49.1 |

| WEDNESDAY, OCTOBER 2 | ||||

| 08:15 | USD | ADP Non-Farm Employment Change | 140K | 195K |

| 10:30 | USD | Crude Oil Inventories | 2.4M | |

| THURSDAY, OCTOBER 3 | ||||

| 10:00 | USD | ISM Non-Manufacturing PMI | 55.1 | 56.4 |

| 21:30 | AUD | Retail Sales m/m | 0.5% | -0.1% |

| FRIDAY, OCTOBER 4 | ||||

| 08:30 | CAD | Trade Balance | -1.1B | -1.1B |

| 08:30 | USD | Average Hourly Earnings m/m | 0.3% | 0.4% |

| 08:30 | USD | Non-Farm Employment Change | 140K | 130K |

| 08:30 | USD | Unemployment Rate | 3.7% | 3.7% |

| 14:00 | USD | Fed Chair Powell Speaks | ||

|

Tony Valente Senior FX Dealer, Global Treasury Solutions |

|||