Monetary Convergence Divergence

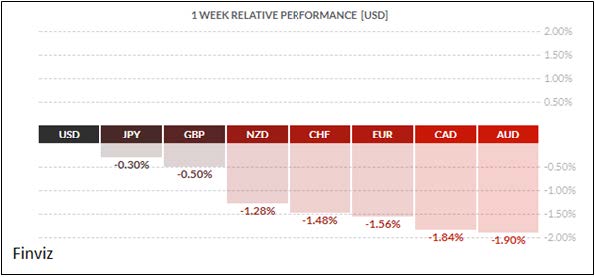

The USD index is enjoying its best weekly gain of the year, up 1.44%, as I pen this. This week’s developments have galvanized the outlook for the USD for the rest of the year. The catalysts were developments within the U.S. and the developments with other central banks that poured cold water on the monetary convergence meme.

The USD index is enjoying its best weekly gain of the year, up 1.44%, as I pen this. This week’s developments have galvanized the outlook for the USD for the rest of the year. The catalysts were developments within the U.S. and the developments with other central banks that poured cold water on the monetary convergence meme.

Friday’s first estimate of Q3 GDP surprised to the upside with a print of 3.0%, putting all fears of a hurricane (Harvey and Irma) induced slowdown in the rear-view mirror. That was the second quarter in a row with 3.0% or higher GDP growth and the fastest pace of back to back growth since the 4.6% and 5.2% revised GDP growth reported for Q2 and Q3 2014. On the surface, this would suggest that the U.S. economy may indeed be starting to overheat and require more interest rate hikes which are very supportive of the USD.

Last Thursday, the Republicans got one step closer to delivering a tax reform package with the passing of the Senate’s version of the 2018 budget resolution. The budget will allow Republicans to pass a tax overhaul that adds up to $1.5 trillion to the deficit through a process known as reconciliation, which only requires 51 votes to pass in the Senate. This clears the way for the House Ways and Means Committee to unveil the tax reform plan next week and schedule a time for the panel to consider it the following week.

The other development that has caused a lift in the USD is the potential one-two punch of Federal Reserve appointments. From all accounts, the next chair of the Fed has come down to current Fed Governor Jerome Powell and Stanford University economist John Taylor. The probability of both being elected Chair and Vice-Chair are very high and Mr. Market is liking the possibility.

These developments have helped the USD index break out of its inverted head & shoulder pattern over the neckline at 94. The momentum indicators are showing that the index has more room to run higher. An obvious target would be the 200-day moving average.

So much for monetary convergence – the developments at other central banks last week helped dispel that myth. The back to back interest rate hikes by the Bank of Canada had set the monetary convergence meme during the summer. However, Wednesday’s BOC decision to stand pat and deliver a dovish outlook helped to reinstate the monetary divergence meme between the Fed and the rest of the global central banks. The BOC kept interest rates at 1.00% and, although it remains confident in the economic outlook, the policy statement explicitly noted that it will take a far more cautious approach to any potential interest rate hikes in the future. They cited NAFTA, mortgage rules changes and the CAD as reasons. None of that will be cleared up by year-end which supports the market’s view that no further rate hikes are likely in 2017. With this in mind, the CAD’s next line of support lies around the 0.77 level. Meanwhile, Mr. Market expects the Fed to raise rates in December and has begun factoring in another in early 2018, thanks to the developments cited earlier with the GDP and tax reform package.

The other key central bank to deliver a dovish tone last week was the European Central Bank. The ECB delivered a dovish taper by announcing that it would cut its asset purchase program (QE) by 30 billion euros starting in January and would continue buying bonds at this pace until September 2018. They also said that they would keep rates at current levels well past the end of QE so the first possible rate hike wouldn’t be until Q4 of 2018. This was enough to crush the euro bulls. The euro broke the neckline of its head and shoulder pattern as the markets realize that while the Fed will be busy raising rates and decreasing its balance sheet in 2018, the ECB will not be doing anything except adding to its balance sheet. There is not a lot of support between here and the 1.14 level. Keeping in mind that the euro makes up 57% of the USD index, the fall in the euro will help to supercharge the rise in the USD index.

Just for good measure, two other central banks reinforced the divergence meme. The central banks of Sweden and Norway both held meeting last week and are in no hurry to change tact. Sweden’s Riksbank reaffirmed that a rate hike is unlikely before the second half of next year despite firm prices and a strong economy. Meanwhile in Norway, the key central bank rate has been 0.50% since March 2016 when it was cut by 25 bps. The Norges bank is currently concerned about institutional restructuring of the country’s wealth fund and not changing its monetary policy stance.

Let’s not forget about the Bank of England as it meets this week. Chances are very high that they may raise interest rates – however, this is not to be taken as start of a new trend but rather the taking back of the post-referendum cut. This is akin to the Bank of Canada’s move to take back the insurance cuts from the oil price shock. Monetary convergence, we’re just not there yet.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, OCTOBER 30 | ||||

| Tentative | JPY | Monetary Policy Statement | ||

| TUESDAY, OCTOBER 31 | ||||

| Tentative | JPY | BOJ Outlook Report | ||

| Tentative | JPY | BOJ Policy Rate | -0.10% | -0.10% |

| 02:30 | JPY | BOJ Press Conference | ||

| 08:30 | CAD | GDP m/m | 0.1% | 0.0% |

| 15:30 | CAD | BOC Gov Poloz Speaks | ||

| 17:45 | NZD | Employment Change q/q | 0.8% | -0.2% |

| 17:45 | NZD | Unemployment Rate | 4.7% | 4.8% |

| WEDNESDAY, NOVEMBER 1 | ||||

| 05:30 | GBP | Manufacturing PMI | 55.9 | 55.9 |

| 08:15 | USD | ADP Non-Farm Employment Change | 191K | 135K |

| 10:00 | USD | ISM Manufacutring PMI | 59.4 | 60.8 |

| 10:30 | USD | Crude OIl Inventories | 0.9M | |

| 14:00 | USD | FOMC Statement | ||

| 20:30 | AUD | Trade Balance | 1.20B | 0.99B |

| THURSDAY, NOVEMBER 2 | ||||

| 05:30 | GBP | Construction PMI | 48.9 | 48.1 |

| 08:00 | GBP | BOE Inflation Report | ||

| 08:00 | GBP | MPC Official Bank Rate Votes | 9-0-0 | 2-0-7 |

| 08:00 | GBP | Monetary Policy Summary | ||

| 08:00 | GBP | Official Bank Rate | 0.50% | 0.25% |

| 08:30 | GBP | BOE Gov Carney Speaks | ||

| 08:30 | USD | Unemployment Claims | 235K | 233K |

| 20:30 | AUD | Retail Sales m/m | 0.5% | -0.6% |

| FRIDAY, NOVEMBER 3 | ||||

| 05:30 | GBP | Services PMI | 53.3 | 53.6 |

| 08:30 | CAD | Employment Change | 13.6K | 10.0K |

| 08:30 | CAD | Trade Balance | -3.4K | |

| 08:30 | CAD | Unemployment Rate | 6.2% | 6.2% |

| 08:30 | USD | Average Hourly Earnings m/m | 0.2% | 0.5% |

| 08:30 | USD | Non-Farm Employment Change | 311K | -33K |

| 08:30 | USD | Unemployment Rate | 4.2% | 4.2% |

| 10:00 | USD | ISM Non-Manufacturing PMI | 58.3 | 59.8 |

|

by TONY VALENTE Senior FX Dealer, Global Treasury Solutions |